Key Performance Indicators – or KPIs – stem from an insight that is most often attributed to Peter Drucker, in his 1954 book titled, ‘The Practice of Management’:

‘What gets measured gets managed’

That attribution may be contested, but the central assertion seems pretty sound. If your organisation measures performance against a specific metric, then its managers feel an incentive to manage their parts of the business, so that they perform well against that metric. KPIs are nothing more nor less than the key – or most valuable – metrics.

It’s often more honoured in the breach than in the observance. But, CSR (or Corporate Social Responsibility) has moved from a ‘nice to have’ add-on to being an obligation many of the world’s largest corporations are embracing.

Yet, while some do it with relish, others display more reticence. And it sometimes seems that no two of them have the same interpretation of what it means. After all, the centuries old profit motive is easy to define and straightforward to measure. But social responsibility… Is that about development, fairness, environmentalism, or what?

Take two electrical engineers. Put one into a management consulting role and the other into academia. Mix them up, and what do you get?

Yes, it is a trick question. Robert Kaplan and David Norton developed a powerful business strategy and performance measurement tool. Indeed, it’s a tool all managers should be aware of and understand: The Balanced Scorecard.

Robert Kaplan & David Norton – Balanced Scorecard

Robert Kaplan

Robert Kaplan was born in 1940 and studied Electrical Engineering at MIT, gaining a BS and then an MS, before moving to Cornell, to take a PhD in Operations research.

He started his academic career directly afterwards, moving to Carnegie Mellon’s Tepper School of Business in 1968. He remained there until 1983, serving as Dean of the school from 1977.

In 1984, Kaplan moved to the Harvard Business School, to take up the chair as Marvin Bower Professor of Leadership Development, which he now holds emeritus.

In 1987, Kaplan, along with William Bruns, first defined Activity Based Costing. It was to become a widely used methodology for gaining control of strategic revenue expenditure in industry. Ironically, it only started to lose ground when a new, more broadly-based approach started to gain popularity.

That approach was the Balanced Scorecard. And this was developed by Kaplan, along with David Norton. They first published their idea in a seminal paper in the Harvard Business Review, in 1992: ‘The Balanced Scorecard—Measures that Drive Performance‘.

David Norton

David Norton was born in 1941. He too studied Electrical Engineering, at Worcester Polytechnic Institute. He moved to the Florida Institute of Technology for an MS in Operations Research, and then to Florida State University for an MBA. He also gained a PhD from Harvard Business School.

Norton’s career was in consultancy, cofounding Nolan Norton & Co in 1975, and serving as president until it was acquired in 1987 by KPMG Peat Marwick. He became a partner, but shortly after the publication of Balanced Scorecard—Measures that Drive Performance‘ in 1992, he founded a new business to promote consulting with the Balanced Scorecard at its heart.

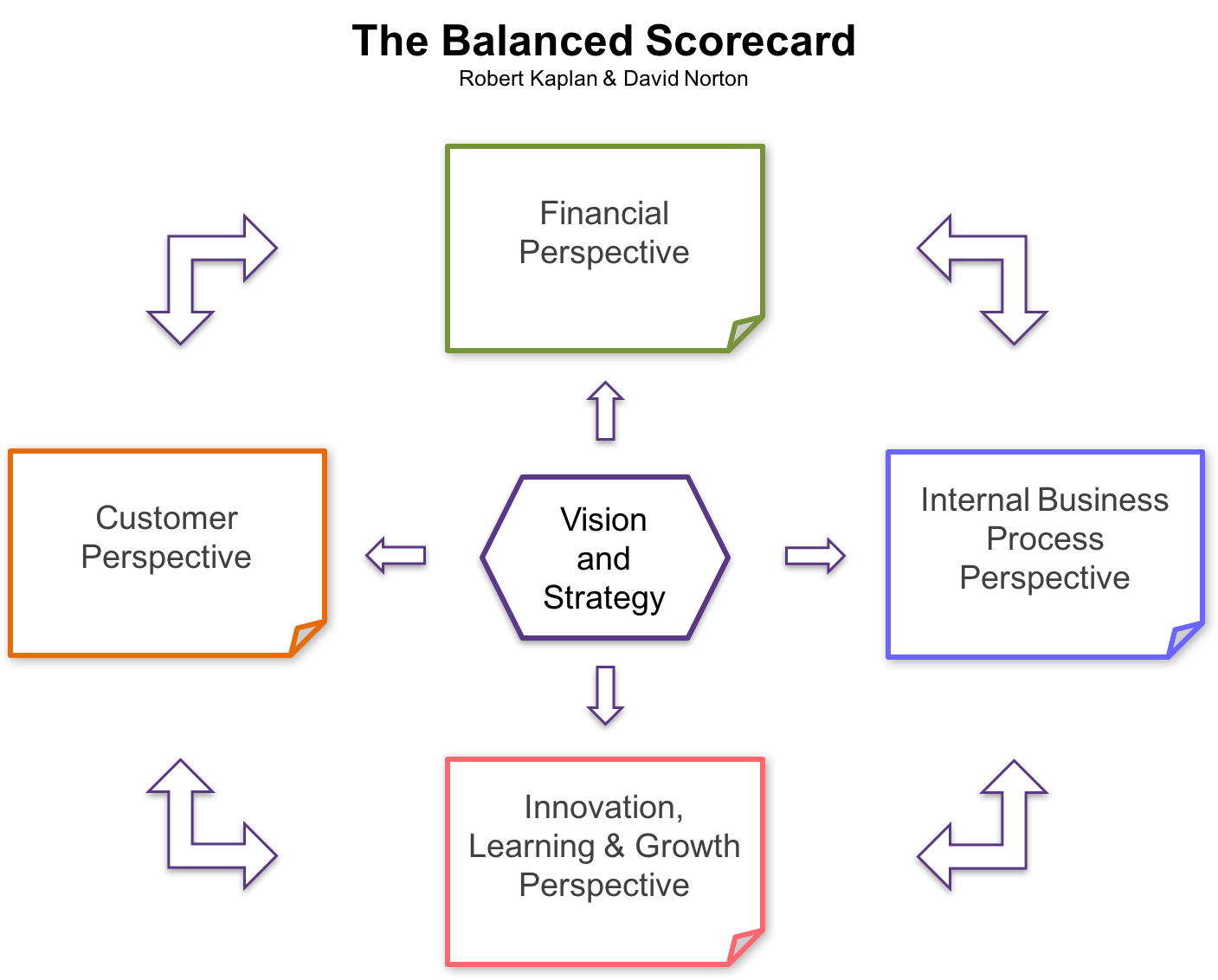

The Balanced Scorecard

We’ve covered the Balanced Scorecard before. But let’s revisit it in some more detail.The idea supposedly came from a conversation David Norton had on a golf course with IBM Executive, John Thompson. Thompson reportedly observed that he needed a scorecard, like the one they used in golf, for running his company.

In a variant metaphor, Kaplan and Norton suggest that it would be an unsafe airplane that had just one gauge in its cockpit. So the idea was born for a scorecard that looks at the business from multiple perspectives. Initially, it is four:

Financial Perspective

Customer Perspective

Internal Business Perspective

Organisational capacity and learning Perspective

Together, the key measures (or KPIs – Key Performance Indicators) under the headings articulate the organisation’s strategic priorities.

Kaplan & Norton – The Balanced Scorecard

The Origins of the Balanced Scorecard

The original idea, however, tracks back to Art Schneiderman in 1987. He went on to work on a research project with Kaplan, and Norton’s firm Nolan Norton. This collaboration led to the publication by Kaplan and Norton in 1992, and their subsequent 1996 book, The Balanced Scorecard: Translating Strategy into Action. It’s now out of print and available only second hand or in digital editions.

One can’t help wondering what happened to Schneiderman – the Pete Best (5th Beetle) of the corporate strategy world. Well, it turns out he’s an independent consultant, and he gives his own history of the first balanced scorecard.

Implementing the Balanced Scorecard

The broad approach to implementing a balanced scorecard is:

Make sure you have a clear vision and strategy

Find the performance categories that best link your vision and strategy to success (Here are some different examples: service standards, thought leadership, marketing activity, performance management, internal morale)

For each perspective, define a small number of objectives that support your vision and strategy

Develop standards or ways to measure progress and build simple systems to monitor and communicate performance against each perspective

Spread the word throughout your organisation that these measures will drive your reward and promotion mechanisms

Monitor performance and compare it with your objectives

Take action to bring performance in line with your objectives

The Legacy of the Balanced Scorecard

As a tool for controlling a business, the balanced scorecard tracks back to Taylorist Scientific Management. However, its flexibility allows managers to monitor and therefore control the measures they choose.

The need for sustainability and for corporations to take their responsibilities to society is a commonplace now. It was not always thus. And one man has played a big part in that transformation: John Elkington.

Very Short Biography

John Elkington was born in 1949, and grew up in England, Northern Ireland, and Cyprus. He studied Sociology and Social Psychology at the University of Essex, gaining his BA in 1970. He then went on to gain an MPhil in Urban and Regional Planning from University College London (where he is currently a visiting Professor – also at Imperial College and Cranfield University).

From there, he worked for four years at a transport and environment consultancy, before spending five years as the editor of the ENDS report (ENvironmental Data Services) from 1978-1983. A prolific writer, Elkington’s first book, The Ecology of Tomorrow’s World, appeared in 1980.

Currently, Elkington serves as Executive Chairman of another business he founded, Volans. This is both a consultancy and think-tank that tries to foresee the future and help clients to make breakthrough changes. He also continues to write books and articles for many publications including frequent articles for the website, GreenBiz. He speaks, and serves on many advisory boards guiding big businesses on sustainability and their corporate and social responsibility.

The Triple Bottom Line

Among the catalogue of ideas that any serious manager or business person must be familiar with is Elkington’s Triple Bottom Line.

He suggested that, in addition to the usual profit-based bottom line measure of a company’s performance, businesses should also prepare bottom line measures in a ‘people account’ and in a ‘planet account’; giving rise to the three pillars of people, profit and planet – another coinage of Elkington’s.

These are often represented as three overlapping circles of concern that clearly represent three views of overlapping stakeholder groups.

‘Profit’ represents the economic imperative felt by owners and shareholders, whose concern is for monetary reward and growth of capital. It refers to the traditional bottom line in a company’s accounts.

‘People’ represents the needs of the organisation’s community and therefore its corporate social responsibilities. A corporation’s social responsibilities extend to all of its stakeholders; not least its employees and the communities within which its facilities sit. This is a big challenge for companies whose shareholders demand that they maximise dividends, whilst its workers are in countries where the state does little to champion their rights.

‘Planet’ represents the natural environment and the part an organisation must play in our joint responsibility for its stewardship. The best organisations treat the environment as a prestigious stakeholder and the worst as nothing more than a source of raw materials and a sink for disposing of waste.

Progress to Date

Pocketblog is not a political commentator, so it must be our readers who assess the progress corporations have made to making the triple bottom line a meaningful commitment. There are examples at both extremes. What is evident, however, is that the challenges facing the world in the coming years are equally great with regards to people and planet, and if too much of our economic activities sacrifice these to the a single profit related bottom line, there may be little left for our grandchildren to spend their profits on.

You May also like the Sustainability Pocketbook

The Sustainability Pocketbook is for managers who want to get involved in this area but are not sure where to start or what they can realistically do.

Share this:

This website requires cookies to provide all of its features. For more information on what data is contained in the cookies, please see our Cookie Policy